June 29, 2026

Publications

Missing Trader Fraud and Misrepresentation: The Case of the Missing GST

In the High Court case of BP Projects Pte Ltd v One Wind Pte Ltd and others [2026] SGHC 105 (“GD”), the 1st to 3rd Defendants were liable in fraudulent misrepresentation to the Claimant in connection with a “missing trader fraud” situation, and were ordered to compensate the Claimant the sum of S$1,747,483.65, being the GST refunds which were disallowed by IRAS.

Key Facts

In mid-2015, Mr. Chua Boon Poon (representative of the Claimant, BP Projects Pte Ltd) met D3 (Mr. Ong Kian Meng) and D4 (Mr. Ong Kian Seng) at City Square Mall.D3 and D4 invited the Claimant to embark on a business venture involving the sale and subsequent on-selling of IT products (e.g. smartphones, software) (“Products”).

Under the proposed arrangement (“Arrangement”):

- BP Projects would first confirm orders from overseas buyers in Vietnam and Malaysia.

- BP Projects would then order the Products from D1 (One Wind Pte Ltd) and D2 (Jueltech Trading Pte Ltd).

- D1 and D2 would then buy the Products from their suppliers and deliver them to BP Projects to on-sell to the overseas buyers.

- Overseas buyers would pay BP Projects the purchase price without GST (as these exports were zero-rated).

- BP Projects would then pay D1 and D2 the purchase price with GST included.

The Claimant alleged that these representations induced them to enter the Arrangement, which later led to financial losses.

Here are 5 key takeaways from this case.

1. Missing Trader Fraud is a Fraudulent Scheme Targeting the GST System

A description of a “missing trader fraud” arrangement was set at [9] of the GD, with reference to IRAS’ website.As IRAS explains on its website:

“Missing Trader Fraud is a fraudulent scheme targeting the GST system. It typically involves fictitious transactions orchestrated by a network of individuals and businesses designed to illicitly claim GST refunds or avoid tax obligations.

Perpetrators of the Missing Trader Fraud often create chains of sales and purchases transactions involving real or fictitious goods or services. A business upstream in the supply chain typically collects GST from subsequent buyers but vanishes without paying the GST to IRAS. GST-registered buyers downstream in the supply chain then claim from IRAS the GST paid to the upstream suppliers. This results in a loss of government revenue.

To form the fraudulent supply chain, perpetrators may use borrowed identities to register fictitious businesses to enable other entities in the chain to claim fictitious GST refunds from IRAS. Your business could also become a party in the fraudulent supply chain, for example, when you accept offers from perpetrators to buy and sell goods in return for a guaranteed profit with little or no risks.”

(Emphasis in bold added)

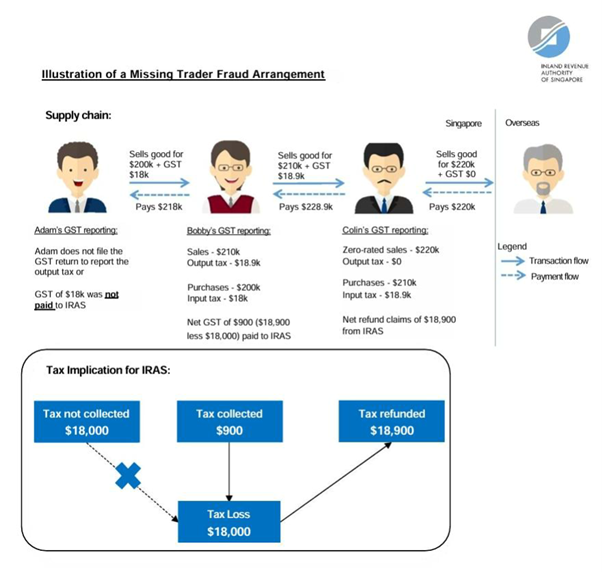

The Court also referred (see GD at [10]) to the following diagram from IRAS’ website which provides an illustration of a “missing trader fraud” arrangement:2. IRAS Took the Position that D1 and D2 were Part of a “Missing Trader Fraud” Arrangement

IRAS investigated the transactions and took the position that D1 and D2 were part of a “missing trader fraud” arrangement (D1 and D2 failed to pay the correct GST to IRAS), and disallowed GST refunds in the amount of S$1,747,483,65 to the Claimant (see GD at [9], [58]).

IRAS imposed various additional tax assessments and penalties on D1 and D2, which also covered the period of the Claimant’s transactions (see GD at [35]).

With reference to the IRAS illustration above, the Claimant was somewhat analogous to the position of “Colin” (save that “Colin” would have been disallowed the GST refund of S$18,900, similar to how the Claimant’s GST refunds were disallowed by IRAS).

3. Two Key Misrepresentations were made by D3, and Attributed to D1 and D2

The two key representations found to be false were:- D1 and D2 complied with all the relevant rules and regulations relating to GST (“Compliance Representation”);

- The Claimant “would have no issues claiming for the abovementioned GST refunds” (“Refund Representation”).

Since D3 had the authority to represent D1 and D2 and did act on behalf of them at the material time, his acts and mental state are properly attributed to D1 and D2 so that they are so liable as well.

In this regard, D3 is the director of D1 and the Operations Manager of D2. On D3’s own account, he “managed the business of both [D1] and [D2]”.

See GD at [12], [23], [31], [64] (read with [3]).

4. Elements of Fraudulent Misrepresentation Were Made Out

The Court set out the elements of fraudulent misrepresentation at [15] of the GD.

The Court went on to find that:

- D3 made the representations, and these were representations of fact (including the Refund Representation, which is a representation of the law, which is also a representation of fact) (GD at [23]-[39]).

- The representations were made with the intention that the Claimant would act upon them (GD at [41]-[43]). The Refund Representation and the Compliance Representation (together with other representations) were undoubtedly material, as they collectively portray the Arrangement as a viable or even tried and tested method of making profits.

- The Refund Representation and Compliance Representation were false (GD at [43]-[51]). Amongst other things, D1 and D2 did not comply with the relevant GST rules and regulations.

- The Claimant relied on the misrepresentations (GD at [52]-[54]). Even though Mr. Chua had conducted very basic research by checking IRAS’ website, nothing indicated that he had any in-depth understanding of the working of GST or that he possessed any tax-related expertise.

- The Claimant suffered losses in reliance on the misrepresentations (GD at [55]-[58]). This was in the form of IRAS disallowing its GST refund claims in the amount of S$1,747,483.65. In this regard, the Court found that the payments the Claimant received from overseas buyers for the Products were consistently less than the sums that the Claimant had to pay D1 and D2, which included GST components. The Claimant, therefore, would only make a profit if it could claim GST refunds and undoubtedly suffered losses from its GST refund claims being disallowed.

The Defendants also attempted to argue that the Claimant’s losses stemmed from regulatory intervention, instead of from their misrepresentations. The Court disagreed. IRAS’ intervention took place because D1 and D2’s failure to pay the correct GST constituted a “missing trader fraud” and not for any other independent regulatory purpose.

- D3 was reckless in making the misrepresentations (GD at [59]-[63]). See Point 5 below.

5. State of Mind: Recklessness Suffices to Establish Misrepresentation

It is important to note that the Court found that D3 acted recklessly rather than with knowledge that the misrepresentations were false.

In this regard, D3’s lack of understanding of how to ensure compliance with GST rules and regulations and the implications of not doing so, which was the complete antithesis of the Compliance Representation and Refund Representation respectively, stretched back to the time when he made the misrepresentations. In other words, D3 made the misrepresentations without caring whether they were true or false. On that basis, D3 acted recklessly in making the misrepresentations.

See GD at [59]-[63].

Conclusion

Recklessness, in the sense of making a misrepresentation without caring whether they were true or false, suffices to meet the requirement of falsehood for fraudulent misrepresentation. Actual knowledge that they were false at the time of making the misrepresentation is not necessary.

It is therefore crucial that key representations of fact (which includes representations on the law) leading up to the entering of business ventures or contracts be made only after checking the accuracy of such facts.

As the Court observed at [1] of the GD, “The tax authorities in Singapore are not shy when it comes to enforcing the payment of taxes that are properly due.”

May contractual parties likewise not be shy about checking their facts when making important representations in business negotiations.